BUYING BONDS - YOU BECOME THE LENDER

A bond is considered a fixed-income instrument because it typically pays a fixed amount of interest, usually semiannually. A fixed-income instrument plays three primary roles in a portfolio: to serve as a liquid reserve in emergencies; to generate stable cash flow; and to provide stability, allowing investors to take on equity risk. Bonds are IOUs issued by borrowers to lenders.

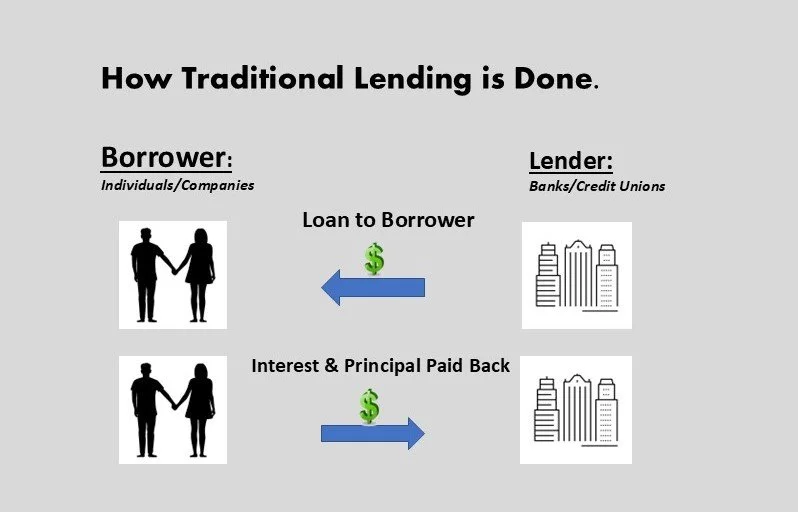

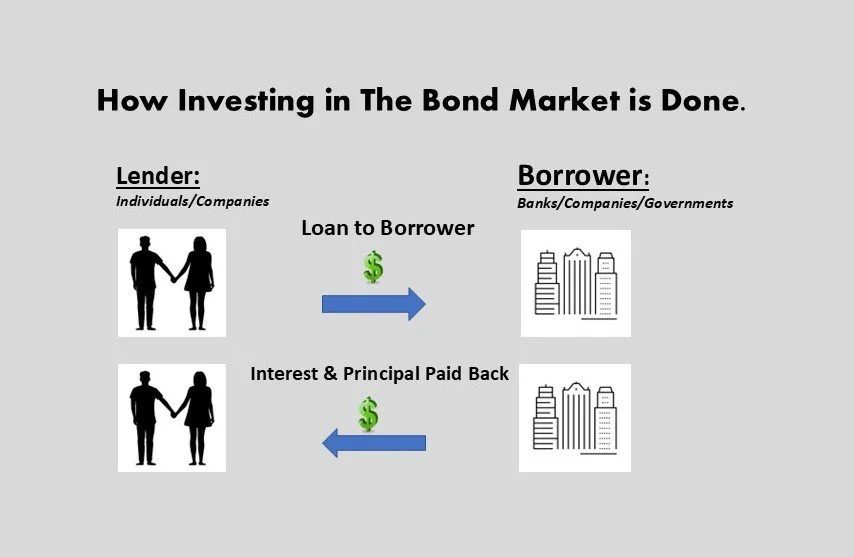

We traditionally think of a loan as originating with a bank (or other investor) and going to the borrower (a person or business) – mortgages, student loans, credit cards, etc. However, when an individual purchases a bond, they become the investor. Bonds are originally purchased in the primary market - directly from the company or government entity borrowing funds. However, most activity takes place in the secondary market – investors buying and selling already-issued securities to other investors.

For example, purchasing a $1,000, 5-year bond with a 3.0% coupon rate will pay $30 in interest per year (two semiannual payments of $15) over the five-year term and return the $1,000 principal at the end of the term.

Traditional Lending Process

Bond Investing Process

Using the illustration above, a bank sets an interest rate that reflects the level of risk it is willing to accept from the borrower. For example, the lowest interest rates go to the least-risky borrowers, based on income, credit score, job security, stability, net worth, and other factors.

For bond investors, the two main factors that determine the expected rate of return on Bonds; Maturity and Credit Quality.

Maturity

Maturity is the length of a bond's term. For example, a 5-year bond pays interest semiannually and repays the principal at the end of the five-year term. Generally, the longer the term, the riskier the investment and, therefore, the higher the expected return. However, there are periods (as recently as 2022-2024) when shorter-term rates exceed longer-term rates, a phenomenon known as an “inverted yield curve.”

Investors demand higher returns for longer maturities because there is more time for uncertainty to materialize—such as inflation, higher interest rates, recessions, wars, and political upheaval. When buying longer-term bonds, investors ask whether they will be rewarded with higher returns for taking on the extra risk associated with longer maturities.

Credit Quality

The U.S. government guarantees its debt. Debt issued by corporations, states, and local governments is not completely default-free, and the lower the credit quality of the bond issuer, the riskier the investment and, therefore, the higher the expected return. There is generally no confusion about this – a borrower that cannot guarantee interest and principal payments will need to pay a higher cost for its money.

Types of Bonds

Government Bonds (U.S. Treasury)

Treasury Bills - Less Than 1-Year Term

Treasury Notes - 2 -10 Year-Term

Treasury Bonds - 20-30 Year-Term

Treasury Inflation-Protected Securities (TIPS)

Corporate Bonds

Investment Grade Bonds – Lower default risk.

High-Yield Bonds – Higher default risk (sometimes called “junk” bonds).

Preferred Shares – Hybrid securities representing company ownership, combining features of both bonds and common stock.

State & Local Governments

Municipal Bonds - Municipal bonds are debt securities issued by states, cities, or local governments to fund public projects. The two primary types are General Obligation (GO) bonds, backed by the issuer's taxing power, and Revenue bonds, secured by revenue from specific projects. They are generally tax-exempt and offer a safer investment than corporate bonds.

Bond Risks

Interest Rate Risk: When market interest rates rise, bond prices typically fall because new bonds offer better returns, making older, lower-yielding bonds less attractive. Shorter-term bonds, such as T-Bills, are less subject to interest rate risk than longer-term bonds. Typically, the longer the bond term, the greater the interest rate risk.

Credit/Default Risk: The possibility that the issuer fails to make interest payments or repay the principal at maturity. All U.S. Government bonds are backed by the Treasury and contain no default risk.

State and local bonds (municipal bonds or "munis") contain default risk, but it is generally very low compared to corporate bonds. While rare, default risk varies significantly between bond types, with revenue bonds riskier than general obligation bonds.

All types of corporate bonds contain some degree of credit risk. The lowest default risk is associated with “investment grade” bonds, which have higher credit ratings from the major rating agencies (Moody’s and Fitch). High-yield bonds are issued by corporations with lower credit ratings. Preferred Shares are another type of corporate debt instrument that contains degrees of credit risk.

Inflation Risk: Inflation erodes the purchasing power of the bond's fixed future cash flows. If I have a bond that pays 3% annually, and inflation is rising at 5%, I am experiencing a loss in purchasing power. The longer a bond's (government or corporate) maturity, the greater the risk that inflation will adversely affect purchasing power.

Reinvestment Risk: The risk that when a bond matures or is called, the proceeds will have to be reinvested at a lower interest rate.

Rating Downgrade Risk: A downgrade in a company's credit rating can cause a sharp decline in the bond's market price.

Individual Bonds v. Mutual Funds (ETF’s): Purchasing individual bonds allows investors to build a “ladder,” an investment strategy that involves buying multiple bonds with staggered maturities to provide steady income while reducing interest rate and reinvestment risk. As each "rung" of the ladder matures, the principal can be reinvested in a new long-term bond, allowing the portfolio to adapt to changing rates. Bond funds are pooled investment vehicles—mutual funds or ETFs—that invest in diverse portfolios of bonds, providing regular income and diversification. They offer easier access to fixed-income markets than individual bonds but carry risks, primarily interest rate and credit risk, as they rarely have fixed maturity dates.

Please feel free to call me (925) 484-1671 or email me to schedule an appointment to discuss my services, your unique situation, or other related matters.

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. Diversification neither assures a profit nor guarantees against loss in a declining market. There is no guarantee that strategies will be successful.