The Roth IRA - Should You Consider Now?

Creating a Roth IRA requires a non-deductible contribution with restrictions, or converting a portion or all of your Traditional IRA to a Roth IRA, which has no dollar limit or income restriction. Many of you may be familiar with the “tax-free” nature of Roth IRA withdrawals, but I would also imagine that the complexities of a Roth IRA cause many to avoid learning more about it. A Roth IRA is a retirement account in which you contribute after-tax money. Because the money is taxed upfront, your investments grow tax-free, and your withdrawals in retirement are tax-free.*

*Must be older than 59½ and the account must be opened (regardless of how many transfers to and from other banks) for at least 5 years.

Retirement planning involves decisions about how to efficiently manage income and expenditures. Effectively analyzing income must account for the tax implications of each decision. The Roth IRA offers significant tax advantages that can generate tax savings year after year, but the primary deterrent is that taxes must be paid upfront on contributions or conversion amounts. Below are some questions and brief answers to help you better understand Roth IRAs.

I have a Traditional or Rollover IRA: What are the differences between these and a Roth IRA?

The primary difference is that ordinary income taxes apply to most distributions from a Traditional or Rollover IRA, whereas Roth distributions are tax-free. However, most contributions to Traditional IRAs are tax-deductible, whereas Roth contributions are not.

What’s the Catch?

Of course, there is a catch to all these wonderful things that can occur with a Roth IRA, and it carries enough weight to make people reluctant to explore the Roth IRA. Essentially, tax must be paid in the year a contribution to a Roth IRA is made or in the year a Traditional IRA is converted, in whole or in part.

For example, Joe makes a $7,500 contribution to his Roth IRA account. The contribution is made with after-tax dollars. If Joe wanted to convert $100,000 from his traditional IRA to a Roth IRA, he would be liable for taxes on the $100,000 conversion amount.

Do I qualify if I am still employed?

In 2026, the maximum standard Roth IRA contribution is $7,500, or $8,600 for those 50 and older. Your ability to make a full or partial direct contribution to a Roth IRA depends on your tax filing status and Modified Adjusted Gross Income.

· Single Filers: You are eligible to make a contribution to a Roth IRA provided your MAGI (Modified Adjusted Gross Income) is below $153,000. The phase-out range ends at a Modified Adjusted Gross Income (MAGI) of $167,999.

· Married Filing Jointly: You are eligible to make a contribution to a Roth IRA provided your MAGI (Modified Adjusted Gross Income) is below $242,000. The phase-out range ends at a Modified Adjusted Gross Income (MAGI) of $251,999.

· There is no income limit to converting a Traditional IRA to a Roth IRA.

The Advantages of A Roth IRA

a) Tax-free withdrawals of interest and appreciation*.

b) Lower taxable income due to non-taxable income could translate into lower income taxes and increase eligibility for certain deductions and credits:

Earned Income Tax Credit, Health Premium Tax Credit, American Opportunity Tax Credit, Medical & Dental Expenses, Student Loan interest, etc.

c) Lower tax liability could translate into more savings or increased spending on other discretionary items.

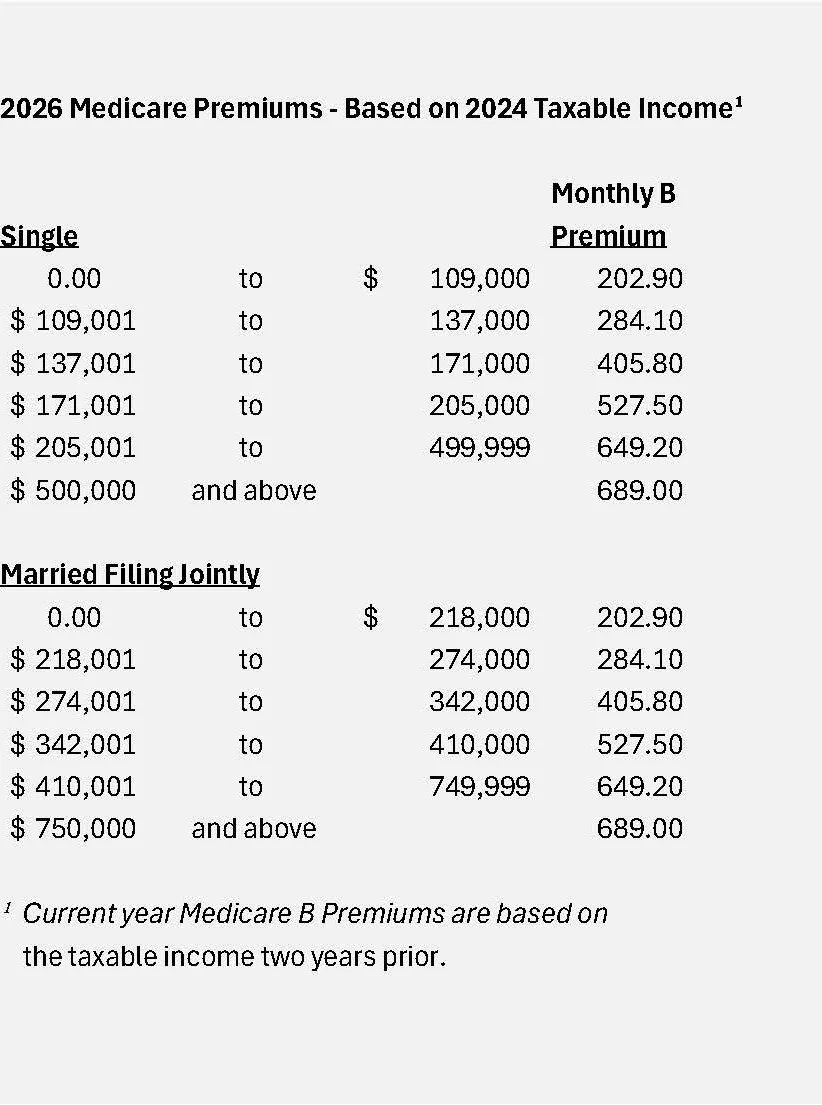

d) Lower Medicare B Premiums, which are based on taxable income two years prior to the current year.

¹ Current year Medicare B Premiums are based on the taxable income for the two years prior.

When Should I Consider a Roth IRA?

a) Anticipation of a higher future tax liability due to projected higher income, reduced deductions and credits, or the expectation of higher national tax brackets. A higher tax rate will increase the amount of tax that is exempt from taxes and help recoup the original tax paid.

b) In addition to a qualified tax-deferred account (401K or IRA), if you have alternative sources of cash, such as savings or a non-qualified taxable account (brokerage), those funds can be used to pay taxes due on a conversion or contribution. Having a non-qualified account (individual, joint, or trust) can provide great flexibility across the different sources of income and the possible tax characteristics of each. However, it is never a good idea to withdraw funds from a qualified account (including the converted IRA) to pay conversion taxes.

c) If most of your retirement savings are in qualified IRAs or 401(k)s, future withdrawals will be taxed at ordinary tax rates. Converting a portion of your IRA funds to a Roth IRA can allow tax-free withdrawals in the future. Lower future taxable income can reduce income thresholds for various tax brackets, deductions, credits, and the taxability of Social Security benefits and Medicare premiums. These potential tax items should be considered to determine whether a Roth IRA is a good financial decision.

d) Since there are no Required Minimum Distributions (RMDs) for a Roth IRA, the balance can accumulate to larger amounts if Roth IRA distributions are minimized or delayed past age 73, which is when RMDs from Traditional IRAs are required to commence. Larger balances will eventually generate larger withdrawals, which could increase the benefit of tax-free income for you and your beneficiary.

e) The Roth IRA can provide tax-free income to a non-spouse beneficiary for up to 10 years after the original owner's death. Traditional IRAs can provide tax-deferred income for up to 10 years, but the income is taxed when withdrawn.

When Should I Not Consider a Roth?

a) If you expect your personal tax liability to decrease in the future due to lower income or fewer deductions, the tax savings from Roth distributions may be minimal, reducing the likelihood of outpacing the original tax paid. For instance, if at the time of conversion your effective tax rate for Fed and State was 30%, but in 10 years, when you plan to take Roth distributions, your effective rate is only 15%, it may take longer for the Roth IRA decision to produce positive value.

b) If you do not intend to distribute much money from the Roth IRA, any tax savings from shielding the smaller amounts will most likely not offset the taxes paid on the contribution or conversion over a retiree's lifetime. Otherwise, keeping the Traditional IRA and avoiding the conversion tax may yield better long-term results. Beneficiaries of Roth IRAs must follow RMD rules and withdraw all funds within 10 years.³

ᶟSee A. Carr’s Blog “Beneficiary IRA Rules.”

Should My Investment Strategy Change With A Roth IRA?

The asset allocation of investments inside either a Traditional or Roth IRA should generally be the same, based on your goals and objectives for your future. However, because withdrawals from the Roth will incur no taxes, a higher risk tolerance inside the account may be appropriate – i.e., higher exposure to equities and other riskier asset classes.

Tax-Exempt investments, such as Municipal Bonds, may not be a priority inside the Roth account because the income from the Roth is tax-exempt. Accepting lower yields for tax purposes may not be an important factor.

Are The Rules For Beneficiaries of Roth IRAs different for a Beneficiary IRA?

The beneficiaries of an inherited Roth IRA follow the same rules as those for an inherited Traditional IRA. See the blog Beneficiary IRA Rules for examples. In summary, a non-spouse who inherits an IRA has 10 years to withdraw all funds – even though the Roth IRA distributions would be tax-free anyway.

What is a Back Door Roth IRA?

A Backdoor Roth IRA is a financial strategy used by high-income earners to legally bypass IRS income limits (see above) and fund a Roth IRA. It involves two steps: making a nondeductible (after-tax) contribution to a traditional IRA, and then immediately converting that money into a Roth IRA.

CLICK FOR FEDERAL PUBLICATION 590 - INDIVIDUAL RETIREMENT ACCOUNTS

What is a Mega Back Door Roth IRA?

A Mega Backdoor Roth IRA is essentially a Back Door Roth with the additional features of using your employer’s retirement plan to contribute more to a Roth than allowed for individual contributions and the ability to convert accumulated balances in an employer-sponsored Roth account to an individual Roth IRA. Much larger accumulations can occur with a Mega Back Door Roth. Your employer’s 401(k) or 403(b) plan must explicitly allow two specific features: after-tax contributions and in-service distributions/conversions.

The analysis required to determine if a Roth IRA makes good financial sense includes input from virtually all areas of financial planning – investments, taxes, distributions, cash flow, and estate planning. I have been a licensed CPA for nearly 39 years and am a Certified Financial Planner. I offer a no-charge consultation, so if you would like to discuss your situation, my services, or this blog, please call me at (925) 484-1671 or email me.

Thank you.

Past performance is no guarantee of future results. Investing risks include loss of principal and fluctuating value. There is no guarantee an investment strategy will be successful.